Why PCI DSS 4.0 Matters for Payment Leaders

For years, PCI DSS compliance has been viewed primarily as a security and compliance function. Organizations allocated budgets for audits, implemented required controls, completed annual assessments, and considered the job done. Payment leaders focused on approval rates, conversion, PSP performance, fraud management, and expansion into new markets, while PCI remained largely in the hands of security teams and auditors.

That separation no longer exists.

PCI DSS 4.0 arrives at a time when the payments landscape has become significantly more complex than the environment previous versions of the standard were designed to protect. Merchants are operating across multiple geographies, integrating with multiple payment service providers, supporting alternative payment methods, leveraging tokenization, and increasingly relying on payment orchestration to optimize performance. Every new payment method, every new provider, and every new market introduces additional complexity into the payment ecosystem.

As a result, PCI DSS 4.0 is no longer simply a compliance framework. It is becoming a strategic consideration that directly affects payment architecture, operational efficiency, customer experience, scalability, and ultimately business growth. The organizations that continue to treat PCI as an annual compliance exercise will find themselves carrying increasing operational burdens. Those that view PCI strategically will discover opportunities to simplify their infrastructure, reduce risk, and build a stronger foundation for long-term growth.

PCI Compliance Is No Longer Just a Security Problem

The biggest misconception surrounding PCI DSS is that it exists solely to satisfy regulatory requirements. In reality, PCI has always been about managing risk. The difference today is that risk extends far beyond the potential for a failed audit.

Every system that stores, processes, or transmits cardholder data creates obligations. Those obligations require monitoring, maintenance, documentation, security controls, testing, and oversight. As payment environments expand, those responsibilities grow alongside them. What begins as a straightforward payment infrastructure can quickly evolve into a complex network of gateways, PSPs, fraud tools, customer support systems, reporting platforms, and internal applications that all interact with payment data in some way.

This complexity has consequences. Development teams move slower because more systems fall under compliance requirements. Security teams spend more time managing controls. Operations teams face greater overhead. New market launches take longer. Vendor onboarding becomes more complicated. In many cases, the cost of managing PCI compliance is not found in audit fees but in the accumulated operational friction created by an overly complex payment environment.

PCI DSS 4.0 acknowledges this reality. Rather than focusing solely on periodic compliance activities, it places greater emphasis on continuous security practices and ongoing risk management. For payment leaders, this means compliance can no longer be delegated entirely to another department. Decisions regarding payment architecture, provider selection, checkout design, and customer payment experiences now have direct implications for security, compliance, and business performance.

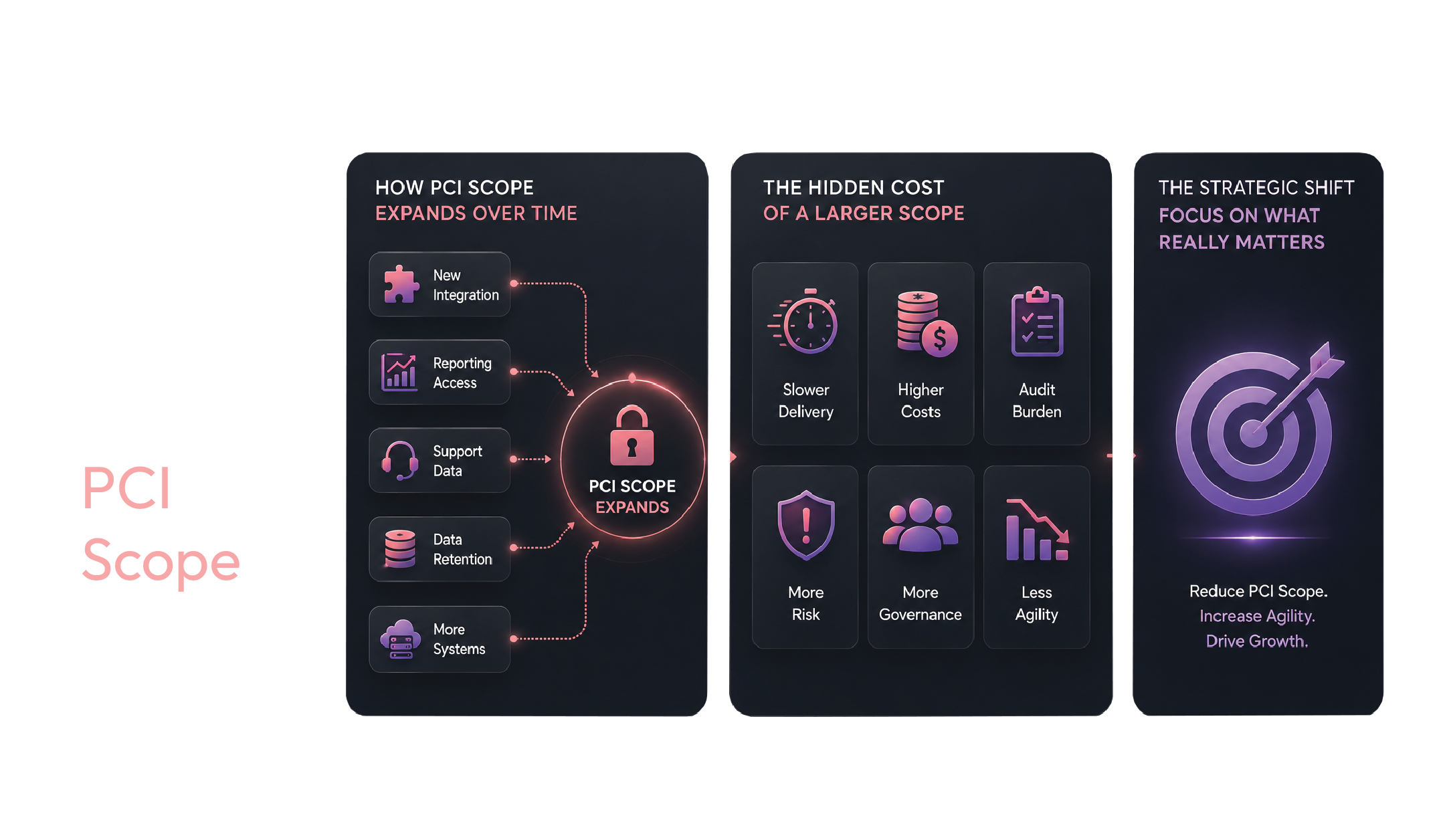

The Hidden Cost of PCI Scope

When organizations discuss PCI compliance, they often focus on requirements. The more important discussion is scope.

PCI scope refers to every system, process, and component that interacts with cardholder data. The larger the scope, the greater the compliance burden. Yet many organizations unintentionally expand their PCI scope over time without recognizing the long-term consequences.

A new PSP integration is added. A reporting system gains access to payment information. Customer support tools begin storing transaction details. Internal databases retain information that is no longer necessary. Individually, these decisions may appear harmless. Collectively, they create a payment environment that becomes increasingly difficult and expensive to manage.

The true cost of PCI scope is rarely visible on a balance sheet. It appears through slower product development, higher operational overhead, more complicated audits, increased security exposure, and reduced organizational agility. Every additional system that touches payment data introduces another potential point of failure and another area that requires ongoing governance.

This is why some of the most sophisticated payment organizations have fundamentally changed the way they approach PCI. Rather than asking how to manage compliance more efficiently, they ask how to reduce the amount of infrastructure that requires compliance in the first place.

That shift in thinking transforms PCI from a defensive exercise into a strategic initiative.

Why PCI DSS 4.0 Changes the Conversation

Previous versions of PCI DSS often encouraged organizations to think about compliance in cycles. Assessments were completed, requirements were reviewed, and compliance activities were concentrated around specific periods of the year.

PCI DSS 4.0 reflects a different reality.

Cyber threats do not operate on annual schedules. Payment environments evolve continuously. New integrations are deployed, customer behaviors change, and fraud tactics become more sophisticated. A static approach to security is increasingly difficult to justify in such a dynamic environment.

The updated standard places greater emphasis on continuous security, stronger authentication controls, ongoing risk assessments, and greater accountability across organizations. While these changes may initially appear to increase compliance obligations, they also encourage businesses to reconsider how their payment infrastructure is designed.

For payment leaders, this is perhaps the most important takeaway. PCI DSS 4.0 is not simply introducing new requirements. It is encouraging organizations to build payment ecosystems that are inherently more secure, more efficient, and easier to manage over time.

The conversation is shifting from compliance management to architecture strategy.

Organizations that recognize this shift early will be in a stronger position to adapt as both security requirements and payment ecosystems continue to evolve.

How Modern Payment Architecture Reduces Risk

One of the most effective ways to improve security is often to reduce exposure.

This principle has become increasingly important as modern payment technologies continue to mature. Tokenization, network tokens, hosted payment fields, secure payment vaults, and payment orchestration platforms all help organizations minimize their interaction with sensitive cardholder data while maintaining flexibility and performance.

Tokenization, for example, allows merchants to replace sensitive payment credentials with non-sensitive tokens. This enables recurring billing, payment routing, and transaction management without repeatedly exposing underlying cardholder information. Similarly, hosted payment environments can shift critical security responsibilities to specialized providers that are purpose-built to manage payment data securely.

Payment orchestration introduces another layer of strategic value. While orchestration is often discussed in terms of approval rates and routing optimization, it can also simplify payment architecture by centralizing integrations and reducing operational complexity. Instead of managing multiple direct integrations across fragmented payment providers, organizations can operate through a more unified framework that improves visibility and governance.

The common theme across all of these approaches is straightforward: reduce the number of systems that interact with sensitive payment data. The fewer systems involved, the lower the risk, the smaller the compliance burden, and the easier it becomes to scale.

Why Scope Reduction Has Become a Competitive Advantage

Historically, PCI compliance was viewed as a cost of doing business. Today, reducing PCI scope has become a competitive advantage.

Organizations with smaller compliance footprints often move faster than their competitors. They can launch products more quickly, enter new markets with less friction, onboard new payment providers more efficiently, and allocate fewer resources to compliance administration.

This advantage becomes even more significant in industries such as iGaming, fintech, eCommerce, and marketplaces, where payment infrastructure plays a central role in customer acquisition and revenue generation. In these sectors, the ability to rapidly adapt payment strategies can directly influence business performance.

A merchant that spends six months navigating compliance challenges before launching a new payment capability is at a disadvantage compared to one that can implement the same capability in weeks. Likewise, a business burdened by excessive operational complexity will struggle to innovate at the pace required by modern markets.

Reducing PCI scope is therefore not simply about lowering compliance costs. It is about creating organizational agility. It allows payment teams to focus less on maintaining infrastructure and more on optimizing performance, improving customer experiences, and driving growth.

The most successful payment organizations increasingly understand that security, compliance, and business performance are not competing objectives. When approached correctly, they reinforce one another.

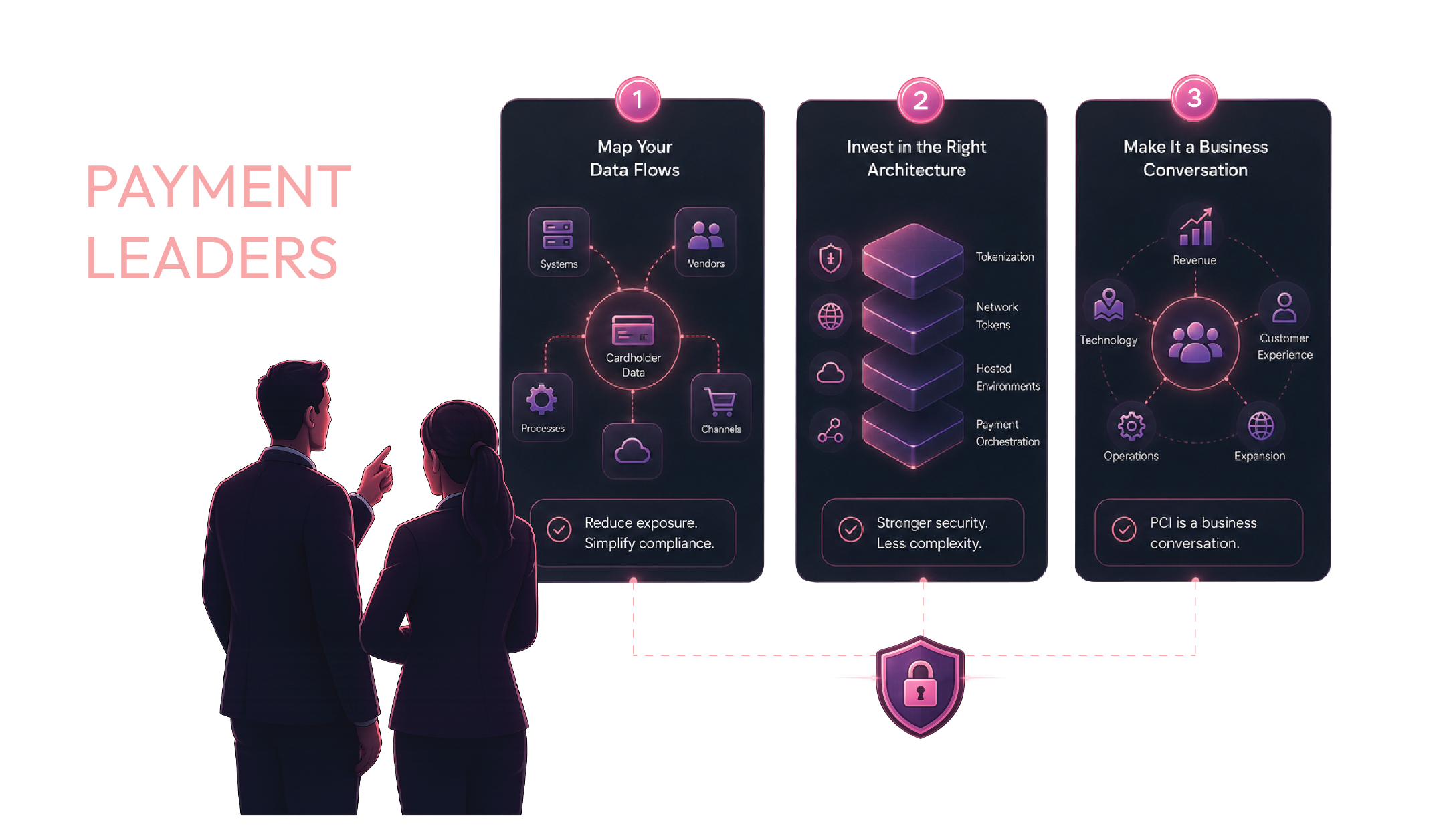

What Payment Leaders Should Do Next

For payment leaders, PCI DSS 4.0 should be viewed as an opportunity rather than an obligation.

The first step is understanding where cardholder data exists within the organization. Many businesses underestimate the number of systems, vendors, and processes that interact with payment information. Mapping these data flows often reveals opportunities to reduce exposure and simplify compliance requirements.

The second step is evaluating whether the current payment architecture supports long-term growth. Technologies such as tokenization, network tokens, hosted payment environments, and payment orchestration should not be viewed solely as operational tools. They are strategic investments that can strengthen security while reducing complexity.

Finally, payment leaders should ensure that compliance discussions extend beyond security teams. Decisions related to payments affect revenue, customer experience, expansion strategies, operational efficiency, and technology roadmaps. PCI is no longer just a security conversation. It is a business conversation.

Final Thoughts

PCI DSS 4.0 represents more than an update to a compliance framework. It reflects a broader shift in how organizations must think about payment security in an increasingly complex digital economy.

The businesses that succeed will not be those that become experts at managing ever-expanding compliance environments. They will be the ones that deliberately design payment ecosystems that minimize exposure, reduce complexity, and support continuous growth.

The question payment leaders should be asking is no longer, “How do we pass our next PCI assessment?”

The better question is, “How do we build a payment infrastructure that requires less compliance effort, carries less risk, and enables greater business agility?”

Because in modern payments, compliance is no longer the destination.

It is the foundation upon which sustainable growth is built.

Let’s Build the Right

Flow for You

Ready to elevate your digital payments? Our team is here to tailor a custom, high-performance infrastructure that scales with your ambitions. Let’s build your next competitive advantage - together.