The Death Of Static Payment Infrastructure

At 10:03 AM, a transaction routes perfectly through a PSP in Germany with a 94% approval rate.

By 2:17 PM, the exact same routing logic begins underperforming because issuer behavior shifts, fraud pressure increases, and authorization patterns change across a specific card segment.

Nothing inside the merchant’s checkout changed.

But the environment around the transaction did.

This is the hidden reality of modern payments.

Every second, the ecosystem underneath a transaction is moving dynamically. Issuer behavior fluctuates continuously. Fraud patterns evolve in real time. PSP performance shifts across regions and transaction types. Authentication pressure changes depending on customer behavior, device patterns, and risk signals. Network conditions fluctuate invisibly beneath the surface.

Yet despite operating in one of the most dynamic environments in digital commerce, much of the payments industry still relies on infrastructure built around static assumptions.

Static routing.

Static fraud thresholds.

Static provider prioritization.

Static optimization cycles.

Static operational logic.

The industry built payment infrastructure for a world that was relatively stable and predictable.

That world no longer exists.

Modern commerce now behaves more like a living system—constantly changing, continuously adapting, and increasingly impossible to optimize through fixed configurations alone.

And this is creating one of the most important structural shifts happening across payments today.

Because the future competitive advantage in payments will not belong to the companies with the largest infrastructure.

It will belong to the companies whose infrastructure adapts the fastest.

Payments Were Built For A More Predictable World

Historically, payment systems were designed around consistency and operational stability.

For years, the industry operated in an environment where payment methods evolved gradually, acquiring relationships remained relatively stable, and fraud patterns changed at a pace businesses could respond to manually. Customer behavior was easier to predict, cross-border complexity was lower, and the overall ecosystem moved slowly enough for periodic optimization to remain effective.

In that environment, static operational models made perfect sense.

Businesses would integrate one or two PSPs, configure routing logic, define fraud thresholds, optimize checkout flows, and monitor performance over time. Once those systems were configured properly, they could remain effective for months or even years with only incremental adjustments.

The underlying assumption was simple:

build the right setup once, optimize periodically, and maintain stability.

That assumption became deeply embedded into the architecture of modern payments.

But digital commerce has evolved far beyond the environment those systems were originally designed for.

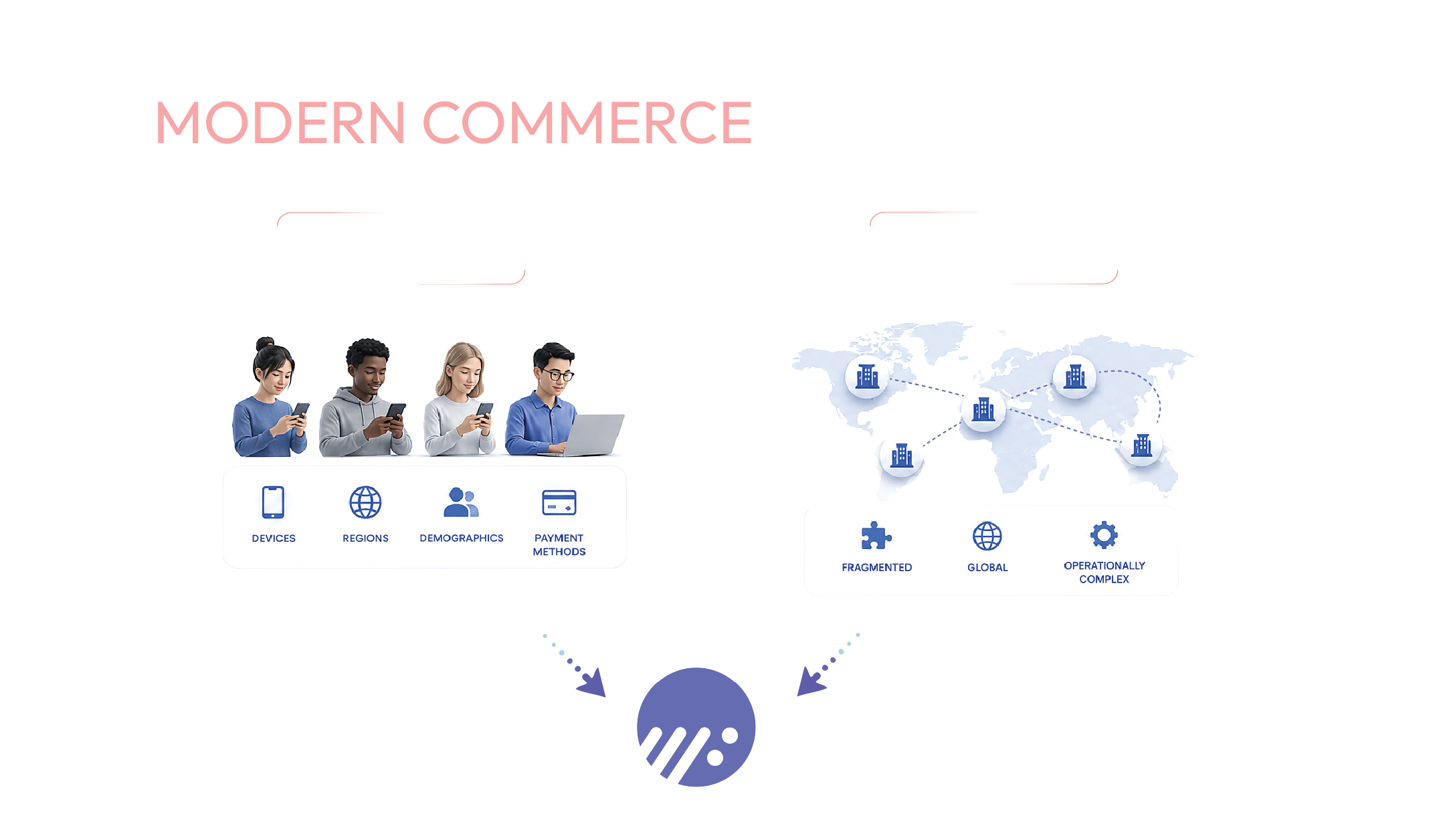

Modern Commerce Is No Longer Static

Today’s payment environment is defined by continuous volatility.

Consumer expectations shift rapidly across devices, regions, demographics, and payment methods. At the same time, businesses themselves are becoming increasingly global, fragmented, and operationally complex.

A single transaction may now involve multiple providers, several fraud systems, tokenization layers, dynamic authentication flows, cross-border routing structures, alternative payment methods, and real-time risk evaluation engines—all operating simultaneously within milliseconds.

This creates an environment where payment performance is no longer fixed.

It is fluid.

A provider that performs exceptionally well in one geography may suddenly underperform in another. Issuer approval behavior can fluctuate during peak transaction periods. Fraud pressure may increase unexpectedly around specific payment methods or markets. Customer friction tolerance may differ dramatically depending on demographic, device, or transaction context.

In many ways, the modern payment ecosystem behaves less like static infrastructure and more like a constantly evolving organism.

Yet many businesses still attempt to manage this environment using fixed operational logic and periodic optimization cycles.

That mismatch is becoming increasingly expensive.

Static Routing Is Quietly Becoming Obsolete

For years, payment optimization focused heavily on routing logic. The industry introduced fallback providers, geographic routing, cascading flows, retries, and acquirer prioritization. At the time, these innovations represented major operational progress because they improved resilience and reduced dependency on single providers.

But modern payment environments are now becoming too dynamic for static routing models to remain sufficient on their own.

Because payment performance no longer changes quarterly or monthly.

It changes continuously.

A routing path that delivers optimal approval performance in the morning may become suboptimal hours later depending on issuer conditions, fraud activity, regional network behavior, transaction type, or changes in customer activity patterns.

This creates a fundamental shift in infrastructure design.

The question is no longer:

“What is the best payment setup?”

The question increasingly becomes:

“How fast can the system adapt when conditions change?”

That is a profoundly different challenge.

Because optimization is no longer periodic.

It is continuous.

Fraud Is Evolving Faster Than Static Systems Can Respond

One of the largest forces accelerating this transformation is the evolution of fraud itself.

Historically, fraud management operated reactively. Businesses would identify suspicious patterns, update rules, introduce new controls, and optimize fraud thresholds over time. Human operations teams could reasonably keep pace with the threat landscape.

But modern fraud environments now operate at machine speed.

Attack vectors evolve continuously through bot-driven attacks, synthetic identities, credential stuffing, automated account takeovers, behavioral spoofing, and increasingly sophisticated AI-generated fraud techniques. Fraud networks adapt dynamically, testing vulnerabilities and modifying attack behavior faster than traditional operational models can respond manually.

This creates enormous operational pressure because businesses now face an increasingly difficult balancing act.

They must reduce fraud exposure without damaging approval rates. They must preserve customer experience while maintaining strong authentication controls. They must minimize friction without increasing operational risk.

Static rule systems struggle under this level of complexity.

Aggressive fraud controls may successfully reduce attacks while simultaneously damaging conversion performance. Relaxed controls may preserve customer experience while increasing exposure. Manual operational adjustments become increasingly unsustainable as transaction volumes scale globally across fragmented payment ecosystems.

This is one of the clearest signals that payments are moving toward adaptive infrastructure models.

Because increasingly, systems must react dynamically rather than rely on predefined assumptions.

Payments Are Quietly Becoming Decision Systems

This is where the industry is entering a fundamentally new phase.

For decades, payments were primarily viewed as processing infrastructure. The objective was simple: move money efficiently from one endpoint to another.

Today, payments are increasingly becoming decision infrastructure.

Every transaction now triggers a growing number of real-time operational decisions. Systems must determine which provider should process the payment, which routing path is currently optimal, how much friction is acceptable for a specific customer, whether authentication should adapt dynamically, and how fraud and conversion should be balanced contextually in real time.

These decisions increasingly determine payment performance long before authorization even occurs.

And this is precisely why the industry is moving beyond simple orchestration toward payment intelligence.

Because access to PSPs alone is no longer enough.

Access is becoming commoditized.

The competitive advantage now comes from decision quality, adaptability, operational visibility, behavioral intelligence, and the ability to optimize continuously in real time.

The infrastructure layer is becoming less about static connectivity and more about dynamic adaptation.

Adaptive Infrastructure Will Define The Next Generation Of Payments

The next generation of payment systems will not behave like traditional financial infrastructure.

They will behave more like intelligent operational networks capable of learning and adapting continuously.

Adaptive payment infrastructure will increasingly reroute transactions dynamically based on live performance signals, optimize authorization behavior in real time, detect anomalies automatically, balance fraud and conversion contextually, and respond instantly to changing issuer or network behavior.

In many ways, payments are beginning to evolve toward autonomous operational models.

Not fully autonomous systems operating without oversight, but infrastructure capable of continuously optimizing itself at a scale human operations teams alone cannot manage manually.

This is one of the most important transformations happening across fintech today.

Because the complexity of modern commerce is now exceeding the capacity of static operational models.

Why This Shift Matters Commercially

For digital businesses, this transition is not simply technical.

It is deeply commercial.

Approval rates, customer experience, retention, fraud exposure, operational visibility, and revenue predictability are increasingly shaped by how adaptive payment infrastructure becomes.

Businesses still operating on static assumptions risk creating invisible inefficiencies across their revenue engine. Small operational delays, suboptimal routing logic, fragmented visibility, unnecessary authentication friction, or delayed responses to issuer behavior can quietly erode conversion and profitability over time.

At Morefin, this shift is becoming increasingly visible across high-volume digital businesses operating in fragmented payment environments.

Companies no longer need only access to providers.

They need infrastructure capable of continuously adapting to issuer behavior, fraud pressure, regional performance shifts, customer expectations, payment method evolution, and operational volatility in real time.

Because modern payments no longer operate in stable environments.

And infrastructure designed primarily for stability struggles in systems defined by constant change.

The Future Of Payments Will Belong To Adaptive Infrastructure

The payments industry is approaching a turning point.

For decades, infrastructure strength was measured by scale: more providers, more integrations, more payment methods, broader acquiring coverage, and larger global networks.

But scale alone is no longer enough.

Because modern commerce no longer operates in predictable conditions.

Consumer behavior changes continuously. Fraud evolves in real time. Issuer performance fluctuates dynamically. Payment methods rise and disappear faster than ever before. Regulatory pressure expands globally. Customer expectations shift almost instantly across markets and generations.

In that environment, static systems inevitably begin to break down.

The next generation of payment leaders will not win because they built the largest infrastructure stacks.

They will win because they built infrastructure capable of adapting continuously without disrupting the customer experience underneath.

That is the real shift happening across the industry.

Payments are evolving from fixed operational systems into intelligent adaptive networks capable of making thousands of real-time decisions dynamically—optimizing routing continuously, balancing fraud and conversion instantly, adapting authentication behavior contextually, and responding to operational volatility automatically.

At Morefin, this transition is becoming increasingly visible across complex digital businesses operating at scale.

Because ultimately, the future competitive advantage in payments will not come from access alone.

Access is becoming commoditized.

The advantage will belong to the companies capable of building intelligence above the infrastructure layer itself.

The companies capable of adapting faster than the environment around them changes.

Because in modern commerce, payment infrastructure is no longer judged only by whether it works.

It is judged by how intelligently it evolves when everything around it does not stand still anymore.

Related articles

Let’s Build the Right

Flow for You

Ready to elevate your digital payments? Our team is here to tailor a custom, high-performance infrastructure that scales with your ambitions. Let’s build your next competitive advantage - together.