Owning Your Payment Infrastructure Is the New Growth Strategy

Owning your payment infrastructure increases approval rates, reduces downtime, accelerates market entry, and improves financial visibility. For high-volume businesses operating in competitive, regulated industries, that control translates directly into higher revenue and stronger positioning.

Most businesses think they've solved payments once the PSP contracts are signed and the gateway is live. Transactions are processing. Customers are paying. Job done.

But there's a gap between having payments and owning your payment infrastructure, and that gap is quietly costing businesses approval rates, customer trust, and revenue every single day.

The businesses growing fastest right now aren't just integrating more PSPs. They're running their payment stack with the same strategic intent they bring to product, marketing, and acquisition. They treat infrastructure as a competitive asset, not a utility.

Here's why that distinction matters, and what it looks like in practice.

What Is the Difference Between Having Payments and Owning Your Payment Infrastructure?

Having payments means you have access: a gateway contract, a few PSP integrations, transactions going through. You can accept deposits and process withdrawals. That's the baseline.

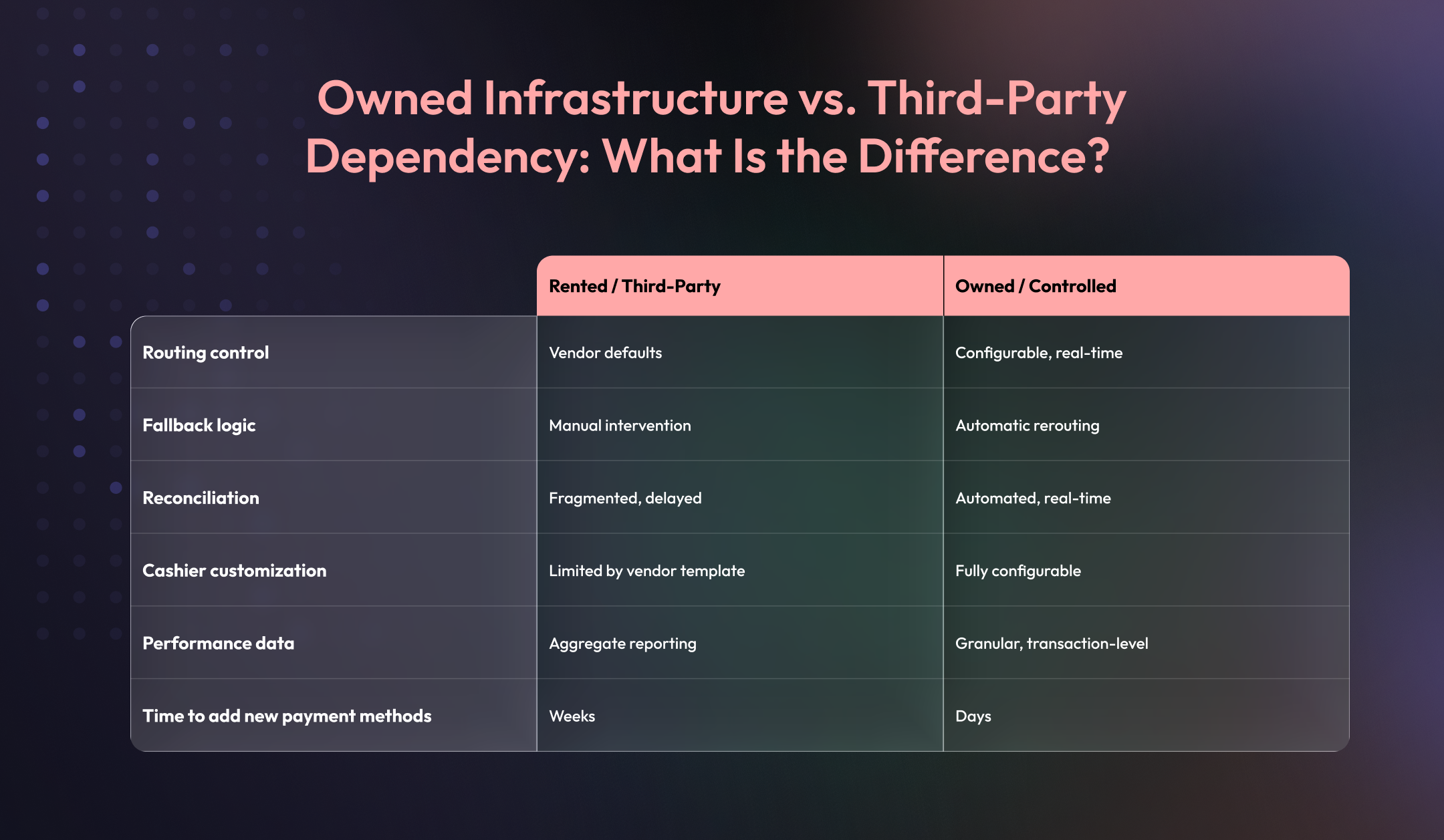

Owning your payment infrastructure means something different. It means you control how transactions are routed in real time. It means you have fallback logic that kicks in automatically when a PSP goes down. It means your checkout experience behaves exactly the way you've configured it, not the way a vendor template dictates. It means your reconciliation data is clean, current, and accounting-ready, not a batch file that arrives three days late.

Think of it like the difference between renting an office and owning the building. You can run a business either way. But ownership changes what you can actually do with the space: how you configure it, how quickly you can adapt it, and what it's worth long-term.

Here's a concrete example. Two operators in the iGaming space — identical PSP setups. One has payment orchestration with intelligent routing and fallback protocols in place. The other doesn't. At peak deposit time on a Saturday night, PSP 1 goes down. For the first operator, traffic reroutes in seconds and players barely notice. For the second, deposits fail until someone manually intervenes. By then, a portion of those players have already gone elsewhere.

That's not a technical difference. That's a revenue difference. And the same dynamic plays out in every industry where payment volume is high, margins matter, and customers expect zero friction.

Why Does Owning Payment Infrastructure Increase Revenue?

Control over your payment infrastructure connects directly to the metrics that drive business performance. These aren't marginal gains. They compound.

Approval rates go up. Smart routing directs each transaction to the PSP most likely to approve it, based on geography, payment method, card type, and real-time performance data. One operator working with MoreFin improved their overall approval rate by 4.2 percentage points within 60 days of implementing intelligent routing, recovering a significant volume of revenue that had previously been lost to default PSP routing.

Uptime becomes a revenue metric. A 99.99% uptime guarantee sounds like a technical specification. But run the numbers: at scale, even a fraction of a percent of downtime during peak hours translates to meaningful lost transaction volume. When your infrastructure is monitored and managed actively rather than through a third-party support queue, you control that exposure.

Data becomes your competitive intelligence. When you own your stack, you own the performance data. Decline rates by PSP, by geography, by payment method, by time of day. That's not reporting. That's your decision-making layer. Without it, you're optimizing blind.

Speed to market compounds. Adding a new payment method in a new market typically takes weeks when you're dependent on a third party's development queue. With the right infrastructure in place, the same move can take days. Over the course of a year, across multiple markets, that gap adds up.

What Are the Risks of Relying on Third-Party Payment Systems?

Most businesses don't realize what they're giving up when they rely entirely on third-party infrastructure, because the costs are invisible until something goes wrong.

No routing control. When a third party owns the routing logic, you get their defaults, not your optimums. You can't A/B test routing strategies. You can't respond to real-time performance signals. You're playing with someone else's rules.

No fallback means no safety net. PSPs go down. That's a fact of the payments industry. Without fallback logic built into your own stack, a PSP outage becomes your outage. Your customers feel it. Your revenue reflects it.

Reconciliation becomes a manual headache. Fragmented settlement data from multiple PSPs, processed on different timelines, in different formats. Finance teams spend hours reconciling what should reconcile automatically. And the data you do get is always behind.

You can't move fast in new markets. Local payment methods are often the deciding factor in customer acquisition in emerging markets. Businesses that don't own their payment stack are consistently the last to add them — because every addition requires a vendor conversation, a development ticket, and a waiting period. By the time they launch, competitors are already established.

You're dependent on someone else's support queue. When something breaks, and it will, your recovery speed is determined by how fast a third party's team responds. That's a fragile position for any business operating around the clock.

How Can High-Volume Businesses Gain Infrastructure Control Without Building In-House?

Owning your payment infrastructure doesn't mean building everything from scratch. For most businesses, that's neither practical nor necessary. What it means is having the right operational model: one that gives you control, visibility, and performance without requiring a dedicated payments engineering team.

In practice, it comes down to four layers working together.

1. Routing intelligence. Real-time smart routing with fallback logic that keeps revenue flowing even when individual PSPs experience issues. This is the core of payment orchestration: the ability to direct each transaction to the optimal path based on live performance data, and to reroute automatically when something goes wrong.

2. Cashier control. Your checkout experience is a conversion surface. The MoreFin Cashier gives businesses direct control over how payments behave at the point of transaction — not a locked vendor template, but a configurable system you can test, optimize, and adjust based on customer behavior and market needs.

3. Reconciliation and reporting. Automated reconciliation that produces accounting-ready reports in real time rather than batch files and manual work. RecoPower handles the complexity of multi-PSP settlement data so your finance team operates on current, accurate numbers rather than chasing discrepancies after the fact.

4. Operations layer. 24/7 monitoring and expert oversight of your entire payment ecosystem. Through Operations as a Service, MoreFin's team manages your payment infrastructure with the same attention and accountability you'd expect from an in-house team, without the headcount.

These four layers aren't separate tools. They're a system. And when they work together, the result is a payment stack that performs like owned infrastructure — because it is.

Owned Infrastructure vs. Third-Party Dependency: What Is the Difference?

How Does MoreFin Make Payment Infrastructure Ownership Accessible?

The strategic case for owning your payment infrastructure is clear. The barrier for most businesses has always been the same: building and running that kind of stack requires specialist expertise, significant development resources, and ongoing operational capacity most teams don't have.

That's exactly the gap MoreFin was built to close.

MoreFin operates as your end-to-end payment infrastructure partner, running your stack with full specialist oversight so you get the performance and control of owned infrastructure without building it from scratch. The process starts with a discovery phase that maps your current payment ecosystem — covering PSPs, geographies, currencies, and customer segments — and identifies exactly where the gaps and opportunities are. From there, the stack is configured around your specific operation, not a generic template.

The result is a payment infrastructure that's genuinely yours to rely on: smart routing, RecoPower reconciliation, the MoreFin Cashier, and round-the-clock payment operations working as a unified system.

If you're ready to move from access to ownership, talk to the MoreFin team.

Frequently Asked Questions

What is payment infrastructure ownership?

Payment infrastructure ownership means having genuine control over how your payments work — not just which PSPs you're connected to. It includes routing logic, fallback protocols, cashier configuration, reconciliation, and real-time performance monitoring. The distinction matters because control over these layers translates directly into approval rates, uptime, and the ability to move fast in new markets.

How does payment orchestration help businesses with high transaction volumes?

Payment orchestration unifies your PSP connections under a single intelligent routing layer. Rather than transactions going through a fixed path, orchestration directs each one to the optimal PSP based on real-time performance data — maximizing approval rates and minimizing the impact of any single PSP failure. You can explore how payment orchestration works at MoreFin here.

What is the difference between a payment gateway and payment infrastructure?

A payment gateway is one component: it processes the transaction between your platform and the PSP. Payment infrastructure is the full stack — the routing logic that decides which gateway to use, the fallback that kicks in when it fails, the cashier that controls the customer-facing payment experience, and the reconciliation layer that keeps your financial data clean. The gateway is a tool; the infrastructure is the system.

Can smaller businesses afford to own their payment infrastructure?

Yes, and this is precisely where the Operations as a Service model changes the equation. You don't need an in-house payments engineering team or years of development work. An OaaS partner like MoreFin runs your infrastructure as a managed service, giving you the performance and control of a fully-owned stack without the headcount or capital expenditure that would traditionally require.

The Bottom Line

The payment layer isn't a back-office function. For any business operating at volume in a competitive market, it's one of the most direct levers on conversion, revenue, and resilience.

The businesses that treat infrastructure as a strategic asset — something to own, optimize, and run with intention — are the ones building durable advantages. The ones that treat it as a commodity are constantly exposed: to PSP failures, to slow market entry, to reconciliation debt, and to approval rates that could be higher.

Ownership isn't just about control. It's about what control enables: faster decisions, better data, higher conversion, and the ability to move when the market moves.

That's what MoreFin is built to deliver. Let's talk about your payment infrastructure.

Related articles

Let’s Build the Right

Flow for You

Ready to elevate your digital payments? Our team is here to tailor a custom, high-performance infrastructure that scales with your ambitions. Let’s build your next competitive advantage - together.