How Different Generations Are Rewriting the Rules of Payments

A Generation Z consumer abandons a checkout because it takes five extra seconds.

A Baby Boomer feels uncomfortable because the payment process happens too quickly.

A Millennial expects the transaction to happen instantly across multiple devices without interruption.

The same payment flow.

Three completely different reactions.

This is the new reality of commerce.

For years, the payments industry believed performance was primarily a technical problem. The focus was infrastructure: faster rails, broader acquiring coverage, lower decline rates, better fraud controls, and more payment methods. Success was measured by whether a transaction could be processed efficiently.

But that assumption is rapidly becoming outdated.

Today, payment performance is increasingly determined not only by infrastructure, but by psychology. Consumers are no longer evaluating payments purely through functionality. They are evaluating them through expectation, behavior, emotional response, and tolerance for friction.

And those expectations are diverging dramatically across generations.

This is creating one of the most important structural shifts the payments industry has faced in decades.

Because modern payment systems are no longer simply financial infrastructure.

They are behavioral infrastructure.

The companies that dominate the next decade of commerce will not necessarily be the ones with the most payment methods or the largest acquiring networks. They will be the ones that best understand how different generations expect money to move.

Payments Have Moved From Infrastructure To Experience

Historically, payments existed in the background of commerce. Their role was operational and largely invisible. If a transaction was approved successfully, the system had done its job.

Speed and reliability mattered, but the payment itself was rarely considered part of the customer experience.

That is no longer true.

In today’s digital economy, payments sit directly at the center of user experience. They influence conversion rates, customer trust, retention, and even brand perception in real time. A payment flow is no longer judged solely by whether it works. It is judged by how it feels.

Consumers increasingly ask questions such as:

- Was the experience instant?

- Did the payment interrupt the journey?

- Did authentication create friction or reassurance?

- Did the process feel intuitive?

- Did the payment disappear naturally into the experience?

These questions may appear subtle, but commercially they are enormously important. In high-frequency digital environments such as e-commerce, iGaming, fintech, marketplaces, and subscription businesses, even minor shifts in friction tolerance can materially impact revenue performance.

And this is where generational behavior becomes strategically critical.

Different generations do not simply prefer different payment methods. They define trust, speed, convenience, and control differently.

The same payment experience that creates confidence for one demographic may create abandonment for another.

Baby Boomers: Trust Is Built Through Visibility

Baby Boomers grew up in a financial world built around institutions. Trust came from banks, branches, cards, statements, signatures, and visible verification processes. Financial systems were designed to feel structured, procedural, and highly controlled.

As a result, this generation often associates security with visibility.

Additional authentication steps, confirmation screens, or verification flows are not automatically perceived as friction. In many cases, they reinforce trust. A payment process that feels “too invisible” can actually reduce confidence because it removes the visible safeguards consumers historically associated with financial security.

This creates an important strategic insight for businesses operating digitally today.

Not all friction is bad friction.

For some customer groups, friction signals protection. For others, it signals inefficiency. Understanding that distinction is becoming increasingly important as businesses optimize payment journeys across multiple demographics.

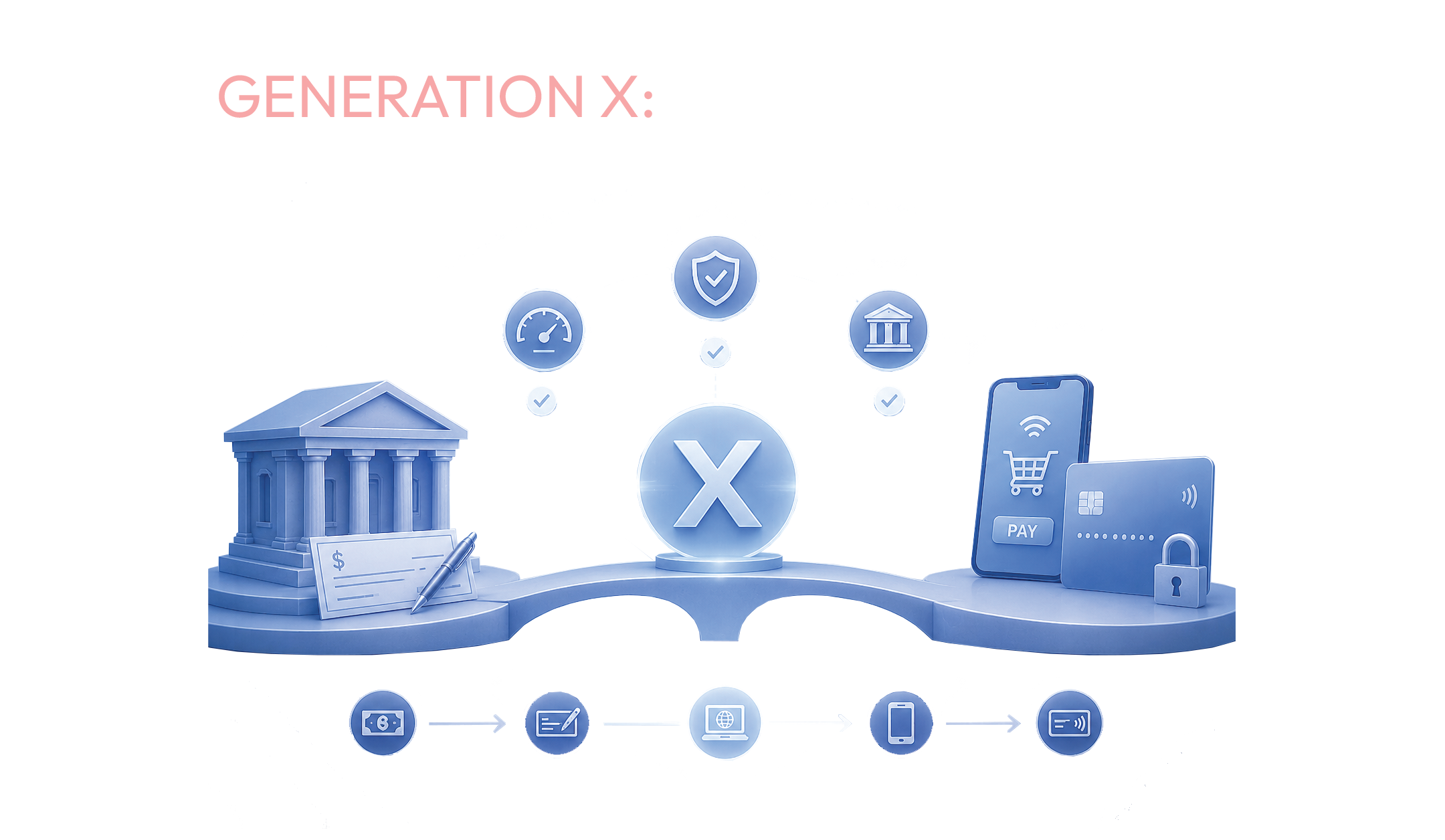

Generation X: The Transitional Financial Generation

Generation X experienced one of the largest financial transitions in modern history. This generation moved from cash, checks, and in-branch banking into online commerce, digital payments, and internet banking during adulthood.

As a result, their relationship with payments tends to balance convenience with caution.

Generation X generally values efficiency, but still prefers systems that feel reliable, predictable, and institutionally grounded. They adopted digital commerce successfully, but they also remember a world before digital finance became dominant.

This creates a hybrid expectation model:

- digital convenience is appreciated

- stability remains essential

- recognizable financial structures still matter

In many ways, Generation X became the bridge between traditional banking behavior and modern fintech behavior.

Millennials: Convenience Became The Standard

Millennials fundamentally changed how consumers interact with financial systems.

This generation accelerated the adoption of:

- mobile wallets

- app-based banking

- subscription commerce

- one-click checkout

- embedded payments

For Millennials, convenience stopped being a differentiator and became a baseline expectation.

This was the generation that normalized the idea that payments should happen naturally inside digital experiences without unnecessary interruption. Consumers increasingly expected financial interactions to operate with the same usability standards as modern technology platforms.

The implications for the industry were enormous.

Payments could no longer compete solely on reliability or acceptance rates. User experience became equally important. Consumers were no longer comparing payment experiences against traditional banks. They were comparing them against Apple, Uber, Spotify, Amazon, and every other frictionless digital platform they used daily.

The standard shifted from financial functionality to digital fluidity.

Generation Z: Payments Should Be Invisible

Generation Z represents the most significant behavioral transformation the payments industry has encountered so far.

For this generation, payments are not expected to feel transactional at all. They are expected to disappear entirely into the experience itself.

Gen Z consumers grew up inside ecosystems defined by immediacy:

- real-time digital interaction

- creator economies

- gaming ecosystems

- mobile-native commerce

- instant access platforms

Their tolerance for interruption is extraordinarily low because digital immediacy is the only reality they have ever known.

A delayed transaction, unnecessary authentication step, or failed payment is not viewed simply as an operational issue. It is perceived as a broken experience.

This distinction is critically important.

Historically, payment infrastructure was optimized for transaction completion. Increasingly, modern consumers evaluate payment systems based on continuity of experience.

Generation Z does not want to “make payments.”

They want uninterrupted outcomes.

This is pushing the industry toward a future where the most successful payment experiences may ultimately become invisible.

The Industry Is Moving From Processing To Decisioning

These generational shifts are driving a much deeper transformation across the payments ecosystem.

For years, the industry focused on processing efficiency:

- successful authorization

- settlement reliability

- fraud prevention

- transaction speed

Today, that is no longer sufficient.

Modern payment systems increasingly need to adapt dynamically based on:

- customer behavior

- transaction context

- geography

- payment method

- device

- risk profile

- friction sensitivity

Static payment flows are becoming obsolete in a world where customer expectations evolve continuously.

This is why the market is rapidly moving toward:

- payment orchestration

- intelligent routing

- behavioral optimization

- adaptive authentication

- payment intelligence

Because the future advantage in payments is no longer access to infrastructure alone.

Infrastructure is increasingly commoditized.

Intelligence is becoming the differentiator.

Why Payment Intelligence Is Becoming Strategic

As businesses scale digitally, payment complexity expands exponentially. More providers, more geographies, more payment methods, more regulations, and more customer expectations create operational environments that static systems struggle to manage effectively.

But the largest challenge is no longer technical complexity alone.

It is behavioral complexity.

Different customers now expect entirely different payment experiences. Businesses that fail to adapt to those expectations create invisible friction that directly impacts conversion, retention, and long-term revenue performance.

At Morefin, this shift is becoming increasingly clear across the industry.

The future of payments is not simply about moving money from one endpoint to another. It is about making intelligent decisions around how payments should behave in real time:

- which provider should process a transaction

- how much friction is acceptable

- when routing should adapt dynamically

- how customer behavior should influence payment logic

- how different user expectations should shape the payment journey

These are no longer purely operational questions.

They are strategic growth questions.

Because increasingly, payment performance is determined long before authorization ever takes place.

The Future Of Payments Will Be Human-Centric

The payments industry is entering a new era.

For decades, infrastructure was the competitive advantage. Then scale became the advantage. Today, intelligence is becoming the advantage.

But that intelligence must increasingly account for human behavior itself.

The companies that succeed over the next decade will not simply process transactions faster than competitors. They will understand how different people expect money to move, how friction affects behavior, and how payment experiences shape digital trust.

Because the future of payments is no longer purely technological.

It is behavioral.

And eventually, the most successful payment experience may be the one consumers never consciously notice at all.

Let’s Build the Right

Flow for You

Ready to elevate your digital payments? Our team is here to tailor a custom, high-performance infrastructure that scales with your ambitions. Let’s build your next competitive advantage - together.