Why Payment Performance Is Decided Before Authorization

In the payments industry, approval rates are often treated as the ultimate measure of success.

They are tracked closely, optimized continuously, and frequently used as a benchmark for operational efficiency. Yet, despite increasing sophistication across the ecosystem, many businesses continue to experience unexplained declines and inconsistent performance.

This raises an important question:

Are we measuring the right moment in the payment lifecycle?

Because while approval happens at authorization, performance is often determined much earlier.

Rethinking Where Outcomes Are Defined

When a transaction is declined, the natural assumption is that the decision lies with the issuer or the card network. After all, they are the ones returning the response.

However, this perspective overlooks a critical aspect of the payment flow.

Before a transaction reaches the issuer, it has already been shaped by a series of upstream decisions. These include the choice of payment service provider (PSP), the acquiring bank, the routing path, and whether the transaction is processed locally or cross-border.

Each of these factors influences how the transaction is interpreted once it reaches the authorization stage.

In practice, this means that two identical transactions—same customer, same card, same amount—can produce entirely different outcomes depending on how they are routed.

The implication is clear:

Payment performance is not only a function of authorization logic, but also of transaction positioning.

The Limits of Network-Level Intelligence

Over the past decade, card networks such as Visa have made significant investments in improving authorization outcomes. Advanced systems, including integrated risk and decisioning frameworks, leverage global data to enhance fraud detection and approval accuracy.

These innovations have undoubtedly strengthened the ecosystem.

However, they operate within a defined scope.

Networks evaluate transactions based on the information and context they receive. They do not control how that context is created. They do not determine which acquirer submits the transaction, nor how it is routed across the payment infrastructure.

As a result, even the most advanced network intelligence cannot fully compensate for suboptimal upstream decisions.

It can optimize within constraints—but it cannot remove them.

The Strategic Role of Routing

This brings greater attention to a layer of payments that has traditionally been viewed as operational rather than strategic: routing.

Routing is often implemented as a set of predefined rules, designed to ensure transactions are processed reliably. But in today’s environment, this static approach is increasingly insufficient.

Modern payment ecosystems are highly dynamic. Issuer behavior varies by geography, regulatory requirements influence processing paths, and provider performance can fluctuate in real time.

Within this context, routing becomes more than a technical configuration. It becomes a decision framework.

Each transaction presents a unique set of variables, and the way those variables are interpreted determines the likelihood of success.

In effect, routing defines the conditions under which authorization takes place.

From Processing to Positioning

Historically, payments have been optimized for execution. The focus has been on ensuring transactions are processed efficiently, systems remain stable, and integrations are scalable.

While these remain important, they no longer provide a competitive edge.

As infrastructure matures, the differentiator shifts from execution to decision-making.

The question is no longer whether a transaction can be processed, but whether it is being processed under the most favorable conditions.

This requires a shift in perspective—from managing payment flows to actively positioning transactions for success.

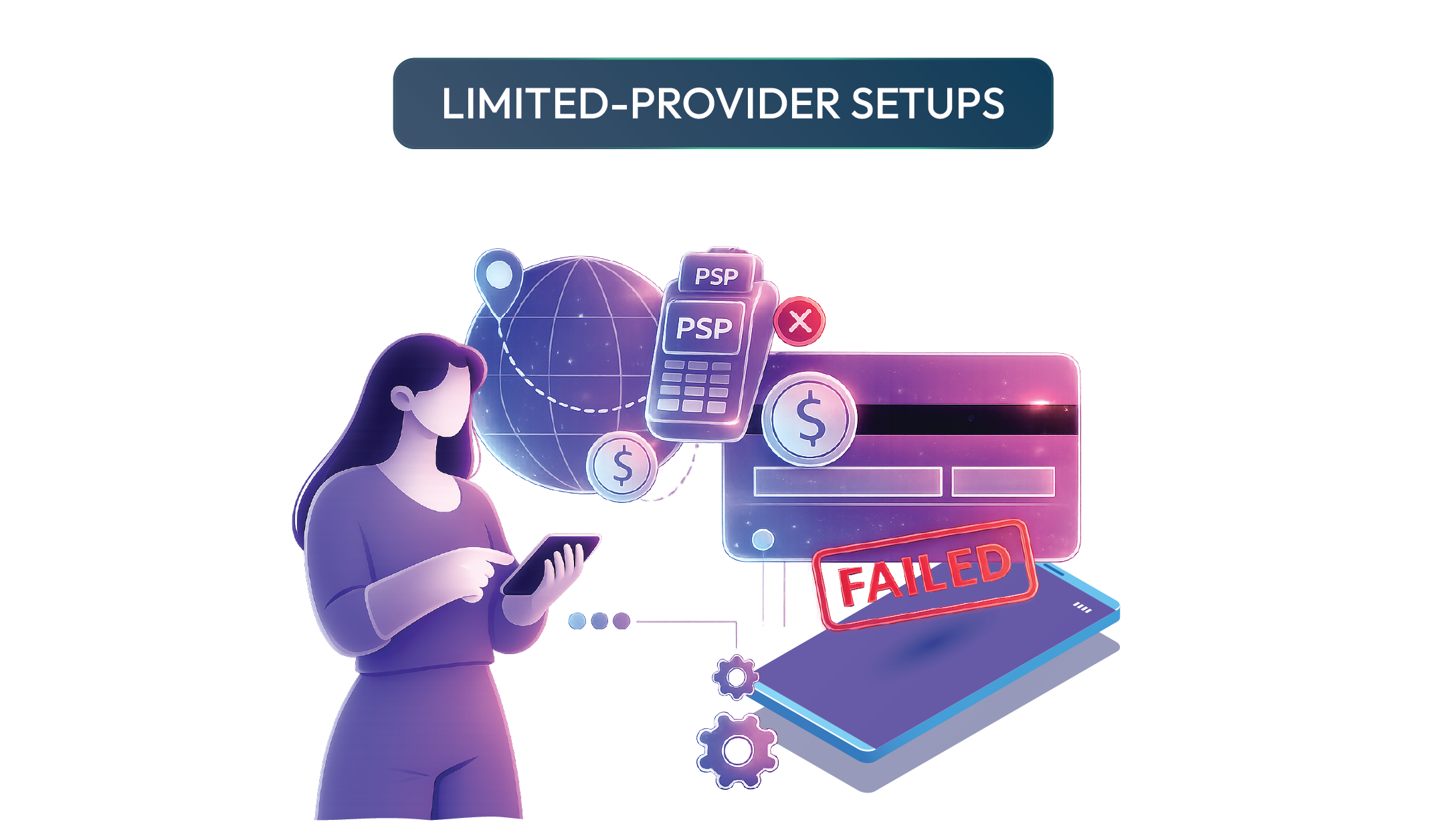

Why Traditional Models Are Under Pressure

Many businesses continue to rely on single-PSP or limited-provider setups. These models offer simplicity and ease of integration, but they also introduce structural limitations.

No single provider can deliver optimal performance across all geographies, issuers, and transaction types. Variability in the ecosystem makes uniform performance increasingly unlikely.

As a result, static configurations often fail to adapt to changing conditions. Transactions are routed in the same way regardless of context, leading to missed optimization opportunities and, ultimately, lower approval rates.

In a dynamic environment, static systems create inefficiencies that compound over time.

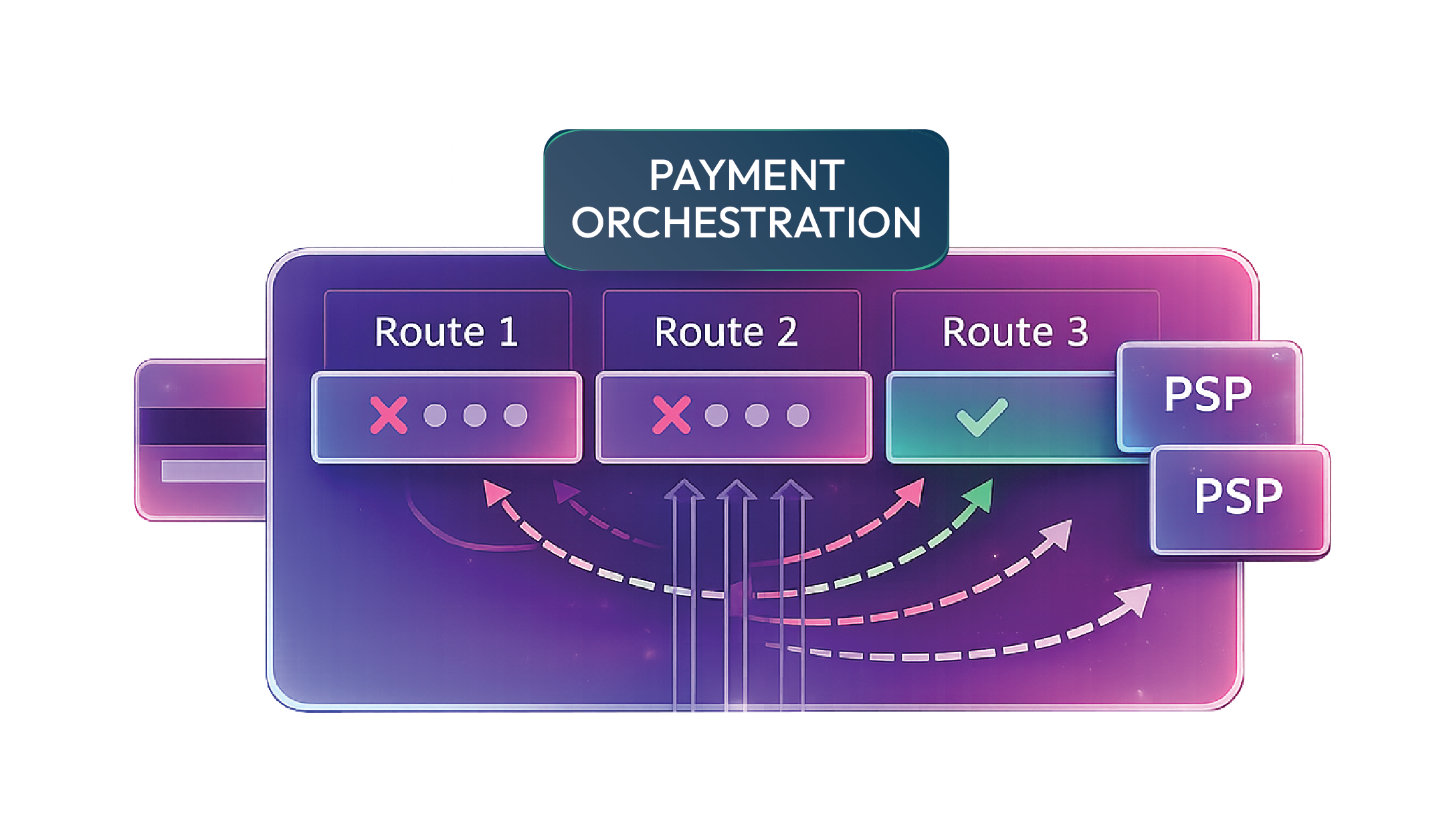

The Emergence of Merchant-Controlled Decisioning

In response to these challenges, a new approach is gaining traction—one that places greater control in the hands of the merchant.

Payment orchestration, when implemented effectively, introduces a layer of intelligence that sits before the network. It enables businesses to evaluate multiple routing options in real time and select the most optimal path for each transaction.

This is not simply about connecting multiple providers. It is about enabling adaptive decision-making.

At Morefin, this approach focuses on aligning routing decisions with real-time performance signals and transaction context. Rather than relying on fixed rules, the system continuously adjusts to optimize outcomes.

The result is a more resilient and responsive payment infrastructure—one that reflects the complexity of the modern ecosystem.

A More Sophisticated Ecosystem Raises Expectations

As the broader payments landscape evolves, expectations are increasing.

Networks like Visa continue to enhance their capabilities, applying more advanced models to transaction evaluation. Issuers are becoming more selective, and fraud systems are more sensitive than ever.

In such an environment, the margin for error narrows.

Transactions that are not optimally positioned are more likely to be declined—not necessarily because they are risky, but because they do not meet increasingly refined criteria.

This reinforces the importance of upstream decision-making.

Conclusion: A Shift in Focus

Payment performance is often viewed through the lens of authorization outcomes. But focusing exclusively on that stage risks overlooking where the most impactful decisions are made.

As the ecosystem becomes more complex and more intelligent, success will depend less on processing efficiency and more on decision quality.

Card networks can optimize how transactions are evaluated.

But businesses must decide how those transactions are positioned.

For organizations looking to improve performance, this represents a shift in focus.

From measuring outcomes

to understanding their causes.

From optimizing approvals

to optimizing decisions before approval is even possible.

A Final Consideration

If payment success is influenced long before authorization, then the key question is not only how transactions are processed—but how they are routed, structured, and positioned from the very beginning.

That is where the next generation of competitive advantage in payments is likely to emerge.

Related articles

Let’s Build the Right

Flow for You

Ready to elevate your digital payments? Our team is here to tailor a custom, high-performance infrastructure that scales with your ambitions. Let’s build your next competitive advantage - together.