The Anatomy of a Modern Payment Stack

Modern payments rarely fail for one big reason. They fail because many small components don’t line up. A modern payment stack is the full set of layers, partners, and processes that move money from checkout to settlement, then prove it in finance reporting. This guide maps every layer, shows how data flows, explains what breaks in real operations, and gives KPIs and evaluation criteria you can use today.

Table of Contents

- What is a modern payment stack?

- Which layers make up a modern payment stack?

- How do PSPs, gateways, and orchestration differ?

- What data flows matter most in payments?

- Where payment stacks fail in real operations (and why)

- Which KPIs show payment stack performance?

- How to evaluate and improve your payment stack

- Key Takeaways

- FAQ

- Conclusion

What is a modern payment stack?

A modern payment stack is the end-to-end system that accepts payments, routes them to the best provider, applies security and compliance controls, moves funds through settlement, and reconciles results into your finance systems. It includes payment methods, PSPs, gateways, acquirers, fraud and 3DS, routing logic, monitoring, and reconciliation workflows.

A “payment stack” is not one vendor. It is an architecture. It includes technology, contracts, rules, and operational routines.

For high-volume, multi-market businesses, a stack is “modern” when it does three things well. It increases approvals without adding risk. It keeps payment operations stable under change. It produces finance-grade truth quickly, not weeks later.

Many payment teams set practical targets like approvals above 90% and daily reconciliation, because the alternative is lost revenue and slow decisions.

Which layers make up a modern payment stack?

A modern payment stack can be viewed as layers: experience (checkout), acceptance (methods and credentials), processing (gateway/PSP/acquirer), decisioning (routing and rules), risk (fraud/3DS/compliance), money movement (capture, settlement, payouts), and finance truth (reconciliation, ledger, reporting). The best stacks define clear ownership and interfaces between layers.

Think of the stack as a “layered map,” not a list of tools. Each layer has a job, inputs, and outputs.

Layer 1: Experience layer (checkout).

Where customers choose a method and authenticate. This includes UI, SDKs, and payment forms.

Layer 2: Acceptance layer (methods + credentials).

Cards, wallets, local methods, stored credentials, and tokenization. Tokenization replaces sensitive PAN data with tokens, reducing exposure and helping scope control. According to PCI Security Standards Council guidance, tokenization systems rely on controlled token-to-PAN retrieval and must protect any components that can recover PAN data.

Layer 3: Processing layer (gateway/PSP/acquirer).

Connectivity to schemes and banks, message formats, authorization, and capture handling.

Layer 4: Decision layer (routing + retries + rules).

Smart routing, cascading, retries, and fallbacks. The key is control: you decide where traffic goes and why.

Layer 5: Risk + compliance layer (fraud, 3DS, SCA).

Fraud tools, velocity rules, device intelligence, and 3DS2 flows. In Europe, Strong Customer Authentication (SCA) applies in defined scenarios like initiating electronic payment transactions, per PSD2 Article 97(1).

Layer 6: Money movement layer (capture → settlement → payouts).

Capture timing, partial captures, refunds, chargebacks, and payout orchestration.

Layer 7: Finance truth layer (reconciliation + ledger + reporting).

Matching provider reports to internal orders, confirming settlement, resolving mismatches, and posting to the ledger.

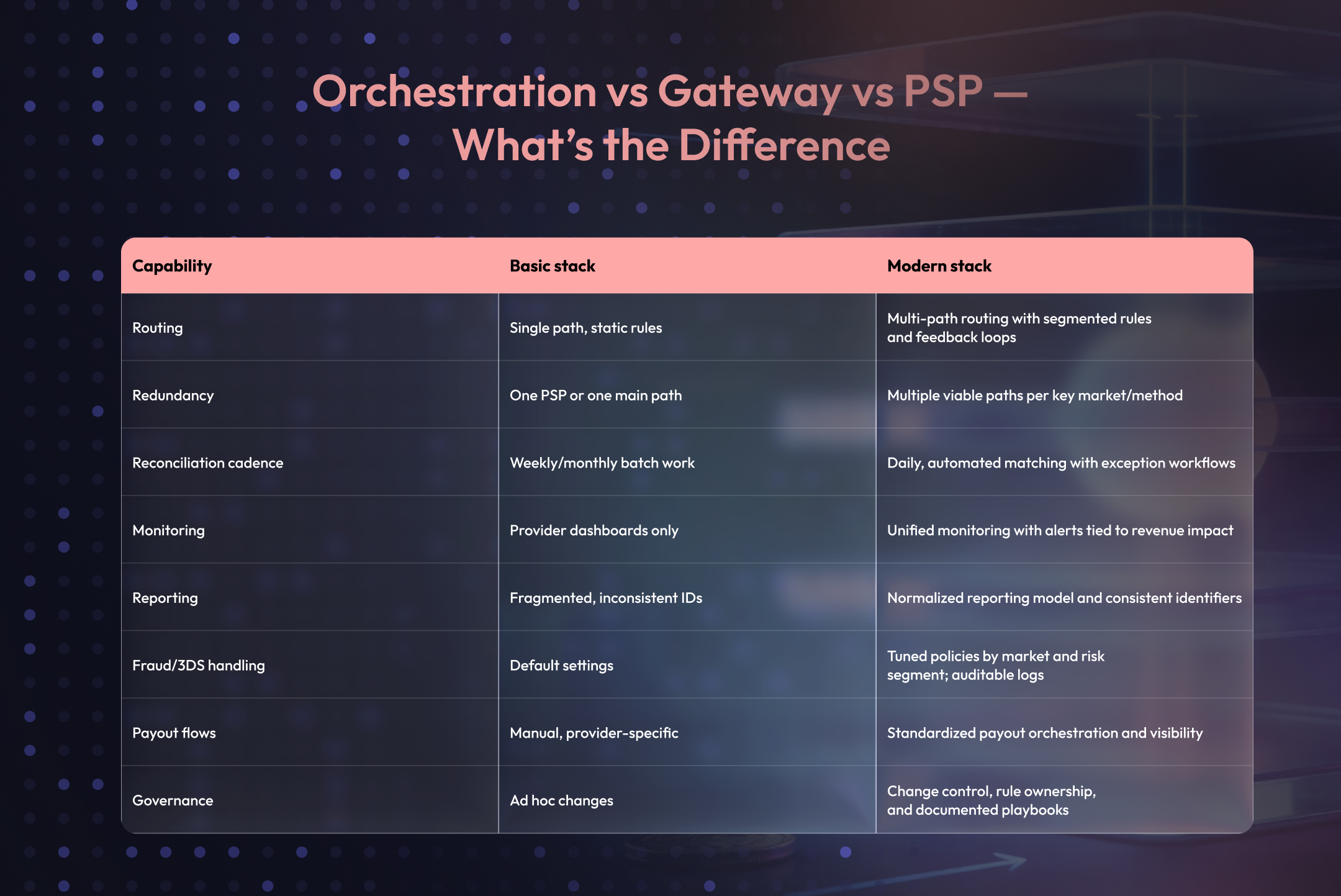

How do PSPs, gateways, and orchestration differ?

A PSP (payment service provider) typically bundles gateway, processing, and method coverage. A gateway is the technical entry point that securely sends payment data and requests authorization.

Payment orchestration is a unifying layer that connects multiple PSPs and tools, then applies routing and rules centrally. Orchestration adds control across providers, not just connectivity.

These terms get mixed because vendors bundle them differently. The easiest way to separate them is by “who owns the decision.”

Payment gateway:

Routes requests to processors/acquirers and returns authorization results. It is often the first “technical hop” after checkout.

PSP:

A commercial and technical package. It may include gateway services, acquiring partnerships, reporting, and method coverage.

Acquirer:

The merchant’s bank (or acquiring institution) that submits transactions to card networks and settles funds.

Payment orchestration:

A middleware layer that normalizes integrations across multiple PSPs and methods. It also centralizes routing, experimentation, and reporting.

The Paypers notes that orchestration is still an intermediary layer, but expectations now go beyond routing. Teams expect more control through rules and settings, and a clearer separation between orchestration and “decisioning.”

What data flows matter most in payments?

The most important payment data flows are: checkout intent → authorization request/response → capture → settlement reporting → reconciliation and ledger posting. You need consistent identifiers across systems, full visibility into declines and issuer response codes, and an audit trail for authentication (3DS/SCA) decisions. Without clean data, you can’t optimize or reconcile confidently.

Most payment issues look like “a decline.” Under the hood, they are usually data problems.

The minimum viable payment data model

You need stable identifiers that survive every hop:

- Order ID / payment intent ID (your system)

- Provider transaction ID (PSP/gateway)

- Acquirer reference (ARN/RRN where available)

- Settlement batch and date

- Method + country + currency

- Authentication result (3DS challenge vs frictionless, liability shift)

The lifecycle you must be able to explain

- Authorize: issuer approves or declines.

- Capture: you confirm the final amount to be settled.

- Settle: funds move through acquiring to your account.

- Reconcile: you match provider statements to internal records.

- Dispute: chargebacks and retrievals adjust outcomes.

Where payment stacks fail in real operations (and why)

Payment stacks fail when they lack redundancy, clear routing logic, and fast operational feedback loops. Common failures include provider outages, misconfigured 3DS or currency settings, issuer-specific decline patterns, retry loops, and reconciliation blind spots that hide losses. The fix is a stack built for change: observability, governance, and daily finance-grade reconciliation.

“Operator view” is where most articles stop short. This is the part your team lives in.

Failure mode 1: One provider becomes a single point of failure

Even short provider degradation can spike declines. If you can’t reroute quickly, revenue drops immediately.

What “good” looks like:

At least two viable processing paths per key market or method. Clear fallback rules. Controlled retries.

Failure mode 2: Routing exists, but the logic is blunt

Routing rules often start as “country → PSP.” That’s not enough. Banks, currencies, amounts, device context, and authentication outcomes matter.

What “good” looks like:

Rules that use signals like issuer country, BIN, method type, amount, and error category. A feedback loop to refine rules weekly, sometimes daily.

Failure mode 3: Authentication friction is mismanaged

In regulated markets, SCA can be required for certain scenarios. But over-triggering challenges can hurt conversion. Under-triggering can raise risk and disputes.

According to the European Banking Authority, PSD2 requires SCA in cases such as initiating electronic payment transactions.

What “good” looks like:

Dynamic 3DS policies by market and risk segment. Clear logging for audits. A plan for exemptions where applicable.

Failure mode 4: Monitoring is fragmented

Teams have many dashboards, but no single operational picture. Issues show up after customers complain.

What “good” looks like:

Real-time alerts tied to business impact: approval drop by method, surge in a decline code, provider latency spikes.

Failure mode 5: Reconciliation lags behind reality

If reconciliation happens weekly or monthly, you learn the truth too late. That delays decisions on fees, routing, and settlements.

Many operators push for daily reconciliation versus multi-week cycles, because it changes how fast finance and payments can act.

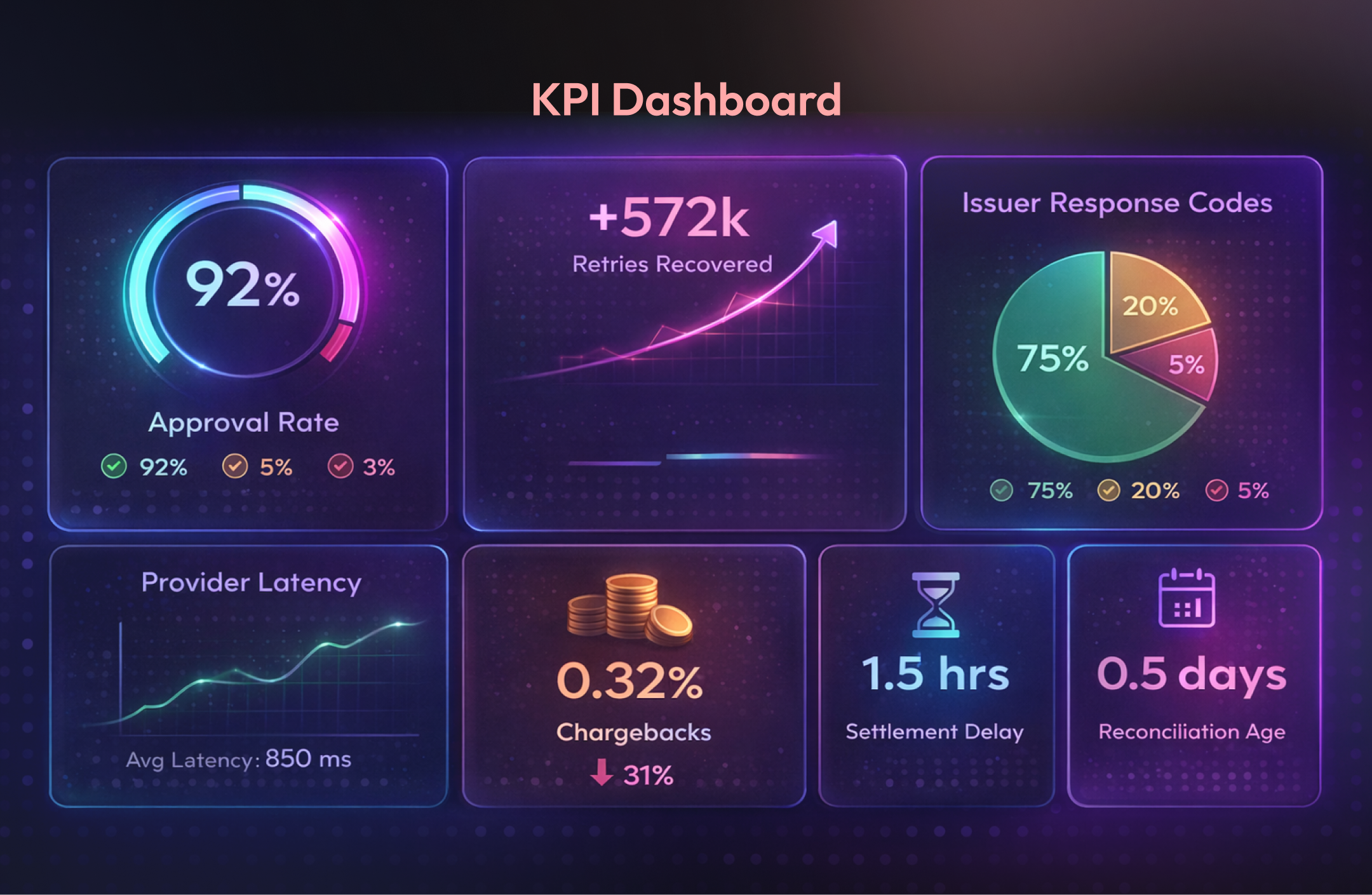

Which KPIs show payment stack performance?

The best payment KPIs connect technical health to revenue and finance accuracy. Track approval rate by segment, soft vs hard declines, retry recovery, authentication challenge rate, provider latency and error rate, cost per successful transaction, chargeback rate, settlement delay, and reconciliation age. KPIs must be segmented by market, method, and provider.

The core KPI set

Revenue and conversion

- Authorization approval rate (by PSP, acquirer, method, country, BIN range)

- Checkout completion rate (intent → success)

- Recovery rate from retries/fallback (how many failures become wins)

Many high-volume businesses use “90%+ approvals” as a practical benchmark for strong performance, especially in card-heavy flows.

Risk and compliance

- 3DS challenge rate and frictionless rate

- Fraud rate (and fraud prevented, if measurable)

- Chargeback rate and dispute win rate

Cost

- Cost per successful transaction (blended fees, FX impact, tooling)

- Provider fee variance vs contract (where overcharging often hides)

Money movement

- Settlement delay (days) by provider and rail

- Payout success rate and **payout latency

- Finance truth

- Reconciliation age (how long items remain unmatched)

- Unmatched amount (absolute and % of volume)

- Status mismatch rate (internal vs provider)

How to evaluate and improve your payment stack

Evaluate your payment stack by measuring control, redundancy, observability, and finance-grade reporting speed. Map your current layers, identify single points of failure, and confirm you can route, retry, and monitor in near real time. Then tighten reconciliation, standardize identifiers, and run controlled routing experiments focused on approval lift and cost per success.

Start with an architecture map. Then use it to drive decisions.

Step 1: Map your current stack (layers + owners)

List every provider and tool, then assign “owner” and “source of truth”:

- Who owns routing rules?

- Who owns fraud policy?

- Who owns reconciliation and ledger posting?

If ownership is unclear, issues will bounce between teams and vendors.

Step 2: Decide what “modern” means for your business

Not every business needs the same depth. But multi-market volume tends to demand:

- Multiple providers for coverage and resilience

- Central routing control

- A single operational view

- Fast reconciliation and reporting

Step 3: Fix the highest-impact leaks first

High-leverage improvements often include:

- Better decline categorization (soft vs hard, issuer vs technical)

- Smarter fallback rules (avoid loops, avoid repeated failures)

- Authentication tuning (reduce unnecessary challenges)

- Daily reconciliation and settlement visibility

Modern payment stack readiness checklist

- You can route transactions across at least two providers in key markets.

- Routing rules support segmentation (country, method, issuer/BIN, currency, amount).

- Retries are controlled and loop-safe (no repeated failures through the same path).

- 3DS/SCA decisions are logged, searchable, and auditable.

- Tokenization is used for stored credentials, with clear scope controls.

- Monitoring alerts exist for approval drops, error spikes, and latency shifts.

- You track issuer response codes and can act on patterns, not guesses.

- Reconciliation is automated daily, with clear exception queues.

- Settlement delays are visible by provider and rail, not discovered late.

- Finance can tie provider statements to internal orders using stable IDs.

- Cost per successful transaction is measurable by market and provider.

- A governance process exists for rule changes and provider onboarding.

Key Takeaways

- A modern payment stack is a layered system, not a vendor choice.

- Orchestration is about control: one place to connect providers and manage routing rules.

- “Good” stacks treat monitoring and reconciliation as first-class layers, not afterthoughts.

- KPIs must be segmented by market, method, and provider to drive action.

- Dai

More Fin Playbook (1)

fast visibility shorten the time from issue → fix.

FAQ

1) What is a modern payment stack?

A modern payment stack is the full set of layers that accept payments, manage routing and authentication, move funds through settlement, and reconcile results into finance systems. It includes providers, tools, rules, and operational routines. The goal is higher approvals with controlled risk and faster financial visibility.

2) What are the main payment stack components?

Typical components include checkout UI, payment methods, tokenization, a gateway, one or more PSPs and acquirers, fraud and 3DS, routing logic, monitoring, reconciliation, and a ledger/reporting layer. Each component has different “sources of truth,” so consistent identifiers matter.

3) What’s the difference between a payment gateway and payment orchestration?

A gateway is the technical connection that sends transactions for authorization and returns results. Orchestration connects multiple gateways/PSPs and gives you centralized control of routing, retries, and reporting. Orchestration is best when you need flexibility across markets and providers.

4) How does routing improve approval rates?

Routing improves approvals by choosing the best provider path for each transaction based on signals like country, method, issuer, currency, and error type. It also enables controlled fallbacks when a provider degrades. The impact is strongest when routing rules are paired with daily performance feedback.

5) What is the payment reconciliation process?

Reconciliation matches what your platform believes happened with what providers and banks report. It usually compares internal orders, PSP transaction records, settlement statements, and fees. The output is a finance-grade view of what was paid, what settled, and what is still missing.

6) What should a payment monitoring setup include?

Monitoring should track approval rate shifts, error spikes, latency, and decline code patterns by provider and market. It should also alert on settlement delays and payout failures. The best setups tie alerts to business impact, so teams act before support tickets pile up.

7) Which KPIs matter most for a Head of Payments or CFO?

Heads of Payments usually focus on approvals, recovery from retries, provider health, and fraud/chargebacks. CFOs also need settlement delay, fee variance vs contract, and reconciliation age. When those KPIs are visible daily, teams can fix leakage faster.

Conclusion

A modern payment stack is a control system. It’s how you protect approvals, manage risk, and turn transaction noise into finance-grade truth. If your stack is missing redundancy, observability, or fast reconciliation, you will feel it as lost revenue. The next step is to own it as a strategic asset — not just map it.

Map your current stack against the layers in this guide, then score it using the readiness checklist.

If you want a second set of eyes, MoreFin can help assess approval drivers, routing opportunities, and reconciliation bottlenecks, then identify quick wins to improve performance. Just contact us for a consultation.

Related articles

Let’s Build the Right

Flow for You

Ready to elevate your digital payments? Our team is here to tailor a custom, high-performance infrastructure that scales with your ambitions. Let’s build your next competitive advantage - together.